December 2025

IN THIS ISSUE

“Bad news is good news”

Trust these numbers?

Stocks and bonds correlations

The Feds Went Passive

This month saw generous seed donations from the Dells, the the Dalios, and others to the newly created Trump Accounts.

In creating Trump Accounts, the government had to make a critical decision - how would these funds be invested? More precisely, which investment strategy and which investment products would provide the greatest benefit to newborns with, in investment-speak, 18 years to maturity?

Well, the government decided low-cost index funds. Not active management.

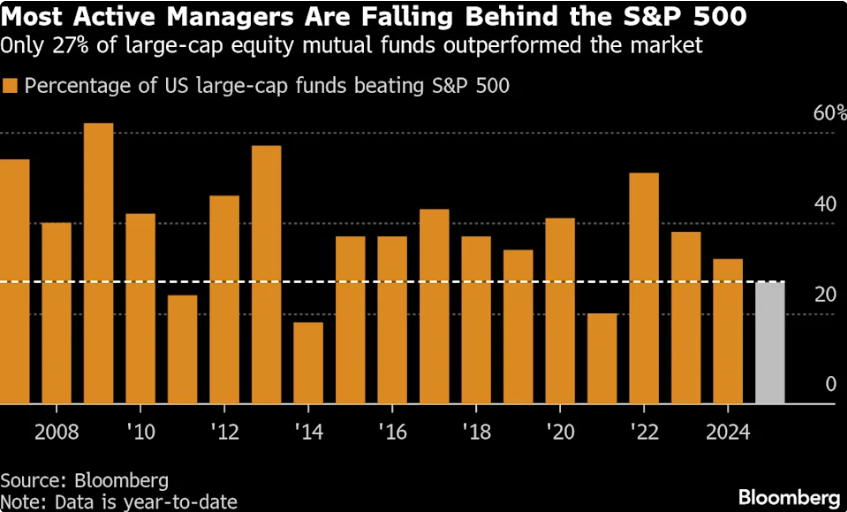

I write often about active versus passive management, consistently detailing how active managers systematically underperform in the long run (e.g. Dead as a Hedge Fund). As S&P Global’s SPIVA reports consistently show, over 15 year time horizons, approximately 90% of all Large-Cap funds underperform the S&P 500 Index. It is no wonder that, as Bloomberg noted this month, Brutal Year for Stock Picking Spurs Trillion-Dollar Fund Exodus:

Around $1 trillion was pulled from active equity mutual funds over the year, according to estimates from Bloomberg Intelligence using ICI data, marking an 11th year of net outflows and, by some measures, the steepest of the cycle. By contrast, passive equity exchange-traded funds got more than $600 billion.

…

The exits happened gradually as the year progressed, with investors reassessing whether to pay for portfolios that looked meaningfully different from the index, only to be forced to live with the consequences when that difference didn’t pay off.

…

Contrary to pundits who thought they saw an environment where stock picking could shine, it was a year in which the cost of deviating from the benchmark remained stubbornly high.

Because Trump Accounts must be held for a long time - until the child turns 18 years old - it is very Likely that America’s next generation would underperform if their capital were entrusted to active managers. In his losing bet with Warren Buffet, Ted Seides learned this lesson the hard way too.

The passive strategy decision also sidesteps significant ethical and governance risks. In my September 2025 issue titled Active Government, I relayed Ken Griffin’s "nauseating" concerns over government picking winners and losers and calling Trump’s approach "crony capitalism". Griffin’s argument is that when the state gets involved in picking favorites, businesses shift their focus from innovation to driving favors in D.C., but by choosing broad-based indexing, the government avoids the risk factors and poor governance that arise when political influences are introduced into corporate decision-making. Sounds similar to Trump Accounts not allowing stock picking, yeah?

It is a pleasant surprise that active management lobbyists and financial industry power players did not exert more influence over the investment products. But these groups are already (still?) trying. For one, the Investment Company Institute (ICI), an association representing the asset management industry, wrote this letter in which, under the guise of “consumer choice”, encourage the Department of the Treasury to broaden the interpretation of “Eligible Investments” to allow other investment products that could include the use of borrowing and derivatives. It is not clear how this recommendation would impact the requirement that the product’s annual fees and expenses also not exceed 0.1% of the fund’s balance - because of course, as funds get more active and more complex, they also get more expensive.

In all, the decision to require a passive strategy in Trump Accounts is a win for the future owners of these accounts. The design protects holders from the performance-sapping traps of active management and ensures their wealth is driven by the broad "American tailwind", not the the whims of active managers.

ONE MORE THING…

“Bad news is good news”. Or in other words, economies are complex, responsive balancing machines. CNBC Daily Open: Once again, bad data is good news for markets

Trust these numbers? Trust these numbers? Economists see a lot of flaws in delayed CPI report showing downward inflation

Stocks and bonds correlations. David Kelly notes: “A revival in inflation concerns in recent years, combined with surging government debt, means that bonds are less likely to rally when stocks fall.”

The information and opinions contained in this newsletter are for background and informational/educational purposes only. The information herein is not personalized investment advice nor an investment recommendation on the part of Likely Capital Management, LLC (“Likely Capital”). No portion of the commentary included herein is to be construed as an offer or a solicitation to effect any transaction in securities. No representation, warranty, or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained herein, and no liability is accepted as to the accuracy or completeness of any such information or opinions.

Past performance is not indicative of future performance. There can be no assurance that any investment described herein will replicate its past performance or achieve its current objectives.

Copyright in this newsletter is owned by Likely Capital unless otherwise indicated. The unauthorized use of any material herein may violate numerous statutes, regulations and laws, including, but not limited to, copyright or trademark laws.

Any third-party web sites (“Linked Sites”) or services linked to by this newsletter are not under our control, and therefore we take no responsibility for the Linked Site’s content. The inclusion of any Linked Site does not imply endorsement by Likely Capital of the Linked Site. Use of any such Linked Site is at the user’s own risk.